|

The Power of TMS CAREspondentWe are a true partner with you.

|

|

DPA Master Servicer

|

|

With co-branding, we service the loans, you keep your clientsWe are a world class national correspondent investor and mortgage loan servicer.

|

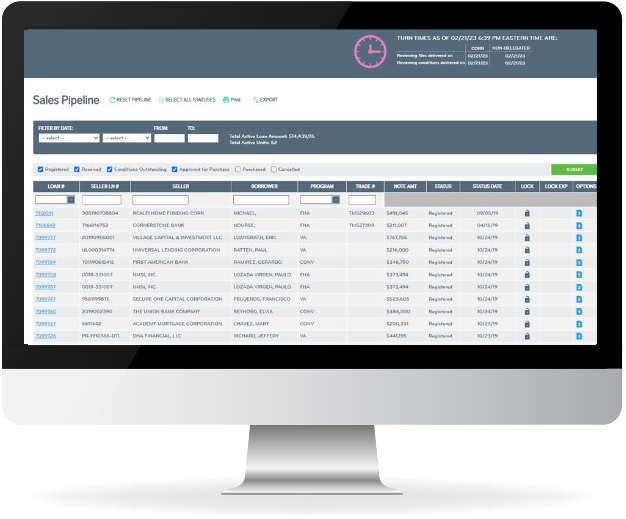

TMS is the only Correspondent lender in the industry to offer guaranteed 24-hour turn times on Initial Funding Review.

TMS is the first to partner with Ellie Mae to bring you Encompass Investor Connect™ – which allows all borrower information to be seamlessly transferred to the investor system with just the push of a button.